Industry down, competitors down, ETP up! What’s the Easy Plan?

Are we seeing a change in travel industry dynamics, or is there something hidden?

Easy Trip Planners (ETP) came out with results for the quarter and year ended 31st Mar 2021 and looks like the numbers were telling a different story than the ground reality. We all know India was under a ferocious attack from the second wave of Covid-19 which began in early March 2021 and we are just about seeing the numbers declining. With this, travel and tourism was last on any consumer’s mind. When we look at results across the industry, travel management companies like Thomas Cook reported poor set of numbers for Q4 2020-21 and hotels like Indian Hotels with the brands like Taj, SeleQtions, Vivanta, Gateway and Ginger too reported losses for the quarter, including the losses in the previous 3 quarters. The same was the case with EIH Ltd (member of Oberoi Group), reporting losses for the previous 4 quarters. When we look at airlines like Indigo and Spicejet, the only listed companies also reported losses for the previous 4 quarters.

Thomas Cook:

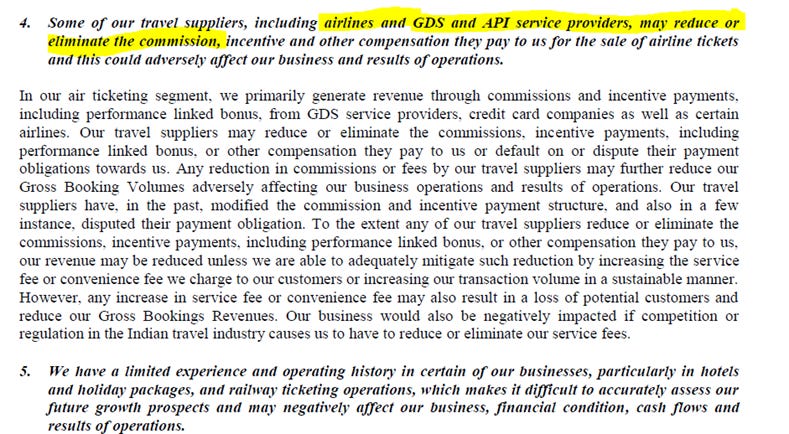

Indian Hotels:

EIH Limited:

Indigo (Interglobe Aviation):

SpiceJet:

Souce: screener.in

We know that markets discount many factors and are forward looking, with many talking about revenge travel, revenge shopping, revenge buying in many of the consumption companies (I sometimes wonder where and how do we coin a word like ‘revenge’ in the midst of a pandemic but guess even Yuval Noah Harari on his book Sapiens said that humans love to travel and they have been traveling since millions of years. May be this is what is driving markets crazy for these stocks). Coming back to the markets and the fact even though travel and tourism related stocks have taken a beating, Easy Trip Planners seem to have found an efficient way of managing the business by staying in profits, or have they?

In this IPO frenzy market, there are many analysts, advisers, youtubers, influencers, grey-market experts etc. who have given detailed analysis of this stock on Twitter, YouTube, Instagram and Facebook when it was listed in Mar 2021. I will leave it for you to pick the best one but one of the videos from the management and the reasons given on the business model and financial statements were remarkably interesting.

An interview with Mr. Prashant Pitti, Co-founder of Ease Trip Planners on Groww YouTube channel caught my attention, which was recorded few weeks before the IPO. The video can be seen on the link

We have mentioned the points which were discussed during the interview (these are not verbatim) and made some observations:

1. ETP doesn’t charge convenience fees (unless one uses a discount code)

One less revenue stream kicked off, must be something else which makes money.

2. FY 2020 annual gross sales or GMV were INR42,000mn in which discounting (coupons, discount code) was 3%, marketing was 0.8%, employee cost 0.7%, admin cost – 0.3%. So the total was 4.8%. Later he also said that the gross margins are less than 10%.

This was quite interesting as when we spoke to few owners and financial heads of several travel companies, large and small, they all said that the margins in this business are very low unless you are only a holiday company where EBITDA margins are more than 12-15%, higher than the air tickets EBITDA margin of around 5%. How they manage to spend 4.8% of GMV or sales with a margin less than 10% and still be profitable is beyond imagination.

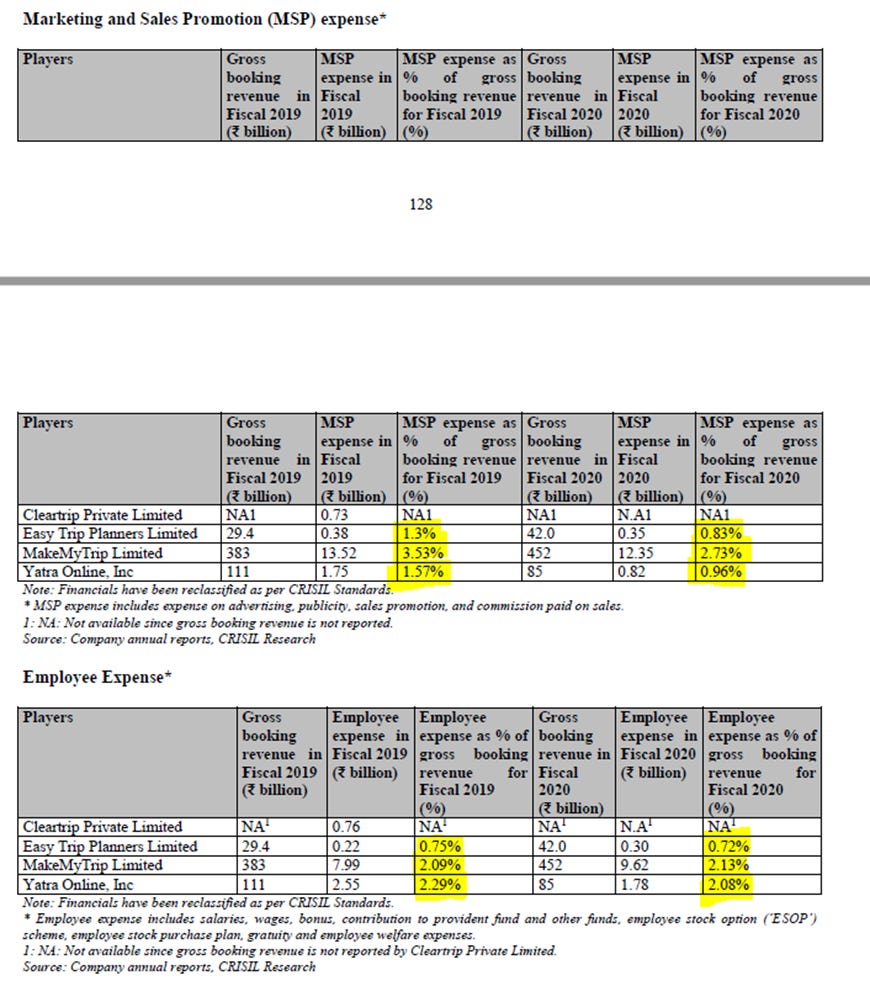

3. In the same breath, he said their competitors total cost spends is 11.4%

We did not come across a single report to justify a 11.4% cost spends by a competitor as the travel industry is quite fragmented and the comparisons are very difficult with different business models. However, we looked at the marketing spends from NASDAQ listed MakeMyTrip, their marketing spends are even higher, but so are the losses since several years. Thomas Cook is not a direct comparison as it has a hybrid model with revenues from forex, holidays, online, corporate travel, hotels, visas etc. and ETP is an online SaaS based business model but the very fact that the revenue numbers of both, MakeMyTrip and Thomas Cook were down by more than 85% tells you how badly bruised this sector has been during this pandemic.

Source: Annual reports

4. The company has a light asset business model. No fancy or swankiest outlets. Most of the office premises are owned.

This is covered well as there are no rentals in income statement and it seems that the promoters have bought the property way back to ensure that the costs are kept minimal. This can be treated as capital infusion and from a business standpoint, one should also calculate the opportunity cost associated with the property purchase. Do we know of any travel company with a low margin business segment and customers which are generally not loyal, have owned premises? Nevertheless, not a substantial point to make so we will move on.

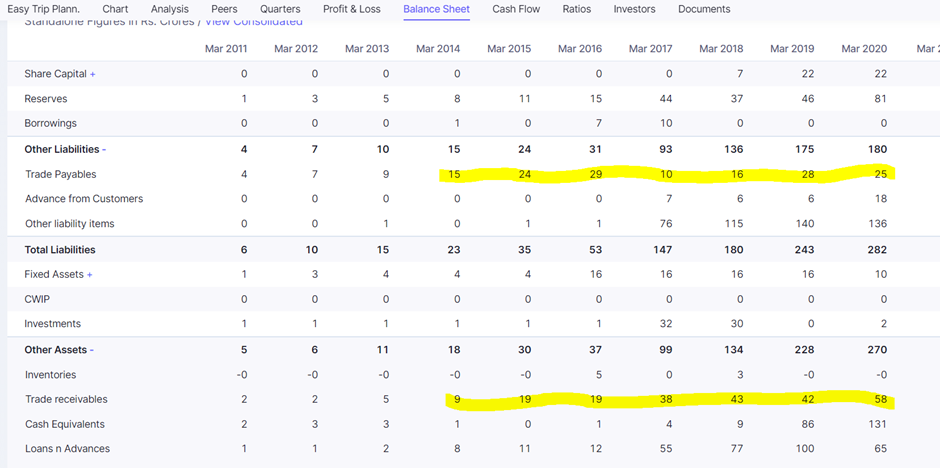

5. Mr. Pitti claimed that the B2B corporate travel segment is only 2.7% of the entire business volume

In a travel segment, when you have a segment which needs credit, the working capital management can really keep you on your toes all the time, not to mention the provisions and write-offs which erodes the profitability. ETP has only 2.7% so they should have negative working capital. Hold on, he did confirm it during the interview, but the balance sheet say something else. Trade receivables are consistently higher than trade payables throughout several years and not just the previous 2 financial years.

Source: Declared results from BSE India and Screener.in

6. The revenue has dropped from INR42,000mn to INR12,000mn, that’s a drop of 71% but the reason they were profitable is because airlines gave better commission, lesser discounting from 3% to 2.1% and increased the strength of technology team from 45 to 69, reduction in reschedule/reissuance team from 30 odd to 3 to 4 employees. Further on 9m EBITDA was INR430mn.

This seems so weird, the drop of 71% in sales is comparatively lesser than industry peers and to post an EBITDA of INR 43cr for 9 months out of which 3 months (Apr 2020 to Jun 2020) were completely washed out, next 3 months (Jul 2020 to Sep 2020) were mostly emergency travel and thereafter there was some demand in international destinations like Maldives and a bit of UAE but still nothing compared to 2019 numbers. Now, lets take a look at revenue numbers from the latest financial results.

Source: Company results

Isn’t it strange that the drop in revenue from operations compared to last year is only 24% and the fact that Mar 2020 quarter sales is lower than Mar 2021 quarter sales. If we go back in memory to the most difficult year, Jan and Feb 2020 had great numbers for the entire industry and it is only after mid-Mar 2021 that the slowdown and eventually the lockdown started.

Company has cash worth INR2,080mn.

Let’s take the financial results and compare:

Source: screener.in

What just happened between Mar 2018 and Mar 2019. Easy IPO planners?

P.S.: I have compared cash flow statements, trade receivables and trade payables before making a point to point comparison.The reason for listing is getting valuation for the company and we don’t have to further spend on marketing. The valuation outside India would have been better.

Oh, well. Come on! This is probably the first time I have come across the reason of listing as a replacement for marketing spends. There are listing expenses as well, right?

Air revenue is 94% of the total revenue

Exactly our point, when a low margin business is 94% of the total and the industry has taken a big hit from Mar 2020, either the numbers don’t make any sense or the company is run so efficiently that it becomes a benchmark in travel and tourism sector. What’s cooking?

We called up few of our known friends and relatives and asked about Easemytrip feedback. Rather than getting a positive response, we were surprised to get a very negative response about their customer care on responses which is exactly opposite to what the founder has spoken about. The sample size in this case was very small so this can be biased, but the responses on Twitter too were not healthy.

Other video:

YouTube Analyst meet before the IPO

Let’s dig deeper in the recent financial statements and also look at the numbers given on Red Herring Prospectus (RHP) by the company before the IPO

1. The borrowings took place in the year 2020-21 as per RHP but why would a company need borrowings when they claim they are EBITDA positive and have generated profits every year.

2. Although customer litigation is a part of travel industry, however, the extent to which this is accounted is quite astounding. Taxation in travel companies is very complex but litigation is also involved in direct tax with an amount of INR356.98 mn

3. Isn’t this exactly opposite of what we heard from the Co-founder?

I am surprised that this reason is even accepted!

5. A low margin business providing loans to movie producers and other companies, including related party?

6. Around 13% business is with B2B (Corporate travel and Travel agents) and the credits are substantial, still a negative working capital claim?

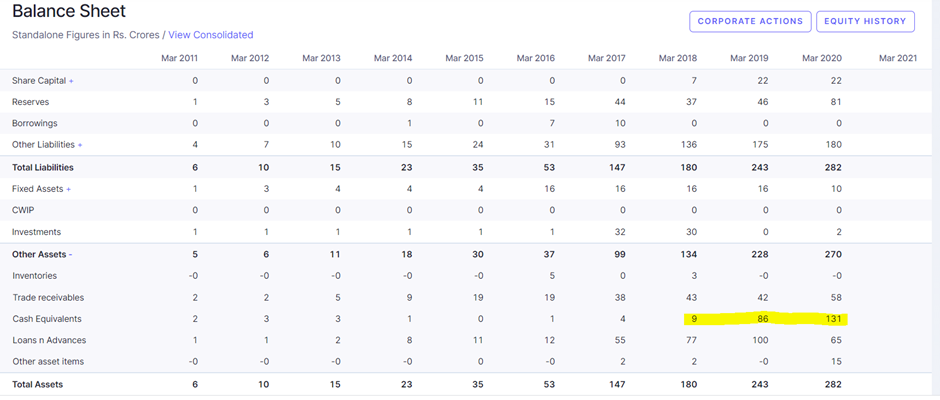

7. Total income increased by 19% but cash and other bank balances almost doubled?

8. Other income driving the business? Salaries have reduced in spite of hiring tech team for automation?

Claims written backs needs to be investigated further as this is not seen in financials of competitors.

9. Customers per employee for ETP is 16,875 whereas for MMT it’s 9,823. There is nothing specific to mention here but the complexity of definition of a customer by all 3 OTAs is quite different.

10. Michael Porter must be wondering where will this business fit in! The circle of competitive rivalry has not affected ETP with no funding. Let us not talk about bargaining power of buyers and suppliers.

How can the efficiency take a hit?

Almost in line with industry peers, isn’t it?

13. Loan before Mar 2020, is that where everything began?

14. Coal business, move business and share trading discontinued. Is this where the funding came from?

Only time will tell if EaseMyTrip is the next CnK!

Disclaimer: I am a SEBI registered Investment Adviser, and the information in this post is only given as an educational case study. This is my opinion and I have every right to be wrong. I, or my family, have no positions in the stock discussed.

I own a micro travel company so it was relatively easy for me to get the information from trust-worthy sources.